Choosing the right auto insurance is important for many reasons. From complying with state law to putting yourself in the best financial position, your auto insurance can affect many aspects of your life. Choosing well can lead to peace of mind for years to come.

But finding the perfect auto insurance for you may be easier said than done without proper research. To compare the different types of auto insurance and choose the best one for your needs, explore this guide from AAA.

How Does Auto Insurance Cover You?

Before you can start your auto insurance comparison, you need to understand the different coverage options that automotive insurance can provide. This helps you identify the type that will best meet your needs.

Auto insurance can cover three types of costs:

- Liability covers the cost of damages you may cause to other people, such as medical expenses and vehicle repairs.

- Physical damage covers costs associated with your vehicle, such as repairs and part replacement.

- Personal covers other costs that problems with your vehicle may create for you, such as medical expenses and lost income.

Each type of insurance will cover you in at least one of these aspects, although some insurance types may cover several of them.

6 Auto Insurance Types

There are six types of insurance to consider getting for your vehicle. Some of these insurance types are optional, while others may be required by law. Pennsylvania, like all other states, has its own state-mandated auto insurance requirements that drivers in the state must comply with.

1. Liability Coverage

Liability coverage, occasionally referred to as third-party coverage, covers the costs of certain damages that were caused by a road accident where you were at fault. Typically, liability coverage is split into bodily injury liability and property damage liability. In most states, including Pennsylvania, drivers are required to be insured for both of these liabilities.

Bodily injury liability helps cover the medical costs that may be incurred by someone you injure in a road accident. In Pennsylvania, every driver must have bodily injury liability that covers the costs of up to $15,000 for one person, or $30,000 for the accident total.

Property damage liability pays toward the cost of any property damage you cause to someone else while driving. This property could include their car, home or anything else they own. The minimum property damage liability limit is $5,000 in Pennsylvania.

2. Collision

Collision insurance helps cover the costs you may have to pay for your vehicle if you hit another vehicle or object. Your insurance can pay toward the repairs your vehicle will need. Alternatively, if your vehicle is irreparable or if it’s cheaper to replace your vehicle, your collision insurance could cover the cost of a new vehicle.

Collision insurance generally has a deductible, which is a minimum amount you pay when you make a claim.

3. Comprehensive

Comprehensive insurance can help cover the costs of damage your vehicle can incur even when you’re not driving it. Common perils that are covered include:

- Theft

- Vandalism

- Fire

- Hail

- Extreme weather events

Comprehensive insurance often includes personal accident coverage for the driver, too. This insurance type usually has a deductible.

4. Medical

This type of coverage can help cover medical costs that a road accident incurs. The insurance usually applies to you and any passengers in your vehicle at the time of the accident. If someone covered by your policy was driving at the time of the accident, it could include them, too.

The bills that medical coverage can go toward vary from one policy to the next, but typical costs include doctor appointments, ambulances, X-rays, surgery and more.

Medical coverage is required in some states, including Pennsylvania, where the minimum coverage limit is $5,000.

5. Uninsured and Underinsured Motorist Coverage

If you suffer damages that were caused by an uninsured or underinsured motorist, this type of coverage could cover your medical bills. An underinsured driver is one who has insurance but can’t cover your medical bills, while an uninsured driver is one who doesn’t have any insurance that can pay toward your medical costs.

Uninsured and underinsured motorist coverage may also cover the repair costs to your vehicle, depending on the state you live in. Whether this type of coverage is required also varies by state, but it’s optional in most.

6. Personal Injury Protection

Personal injury protection (PIP) is similar to medical coverage, but provides more comprehensive coverage. While medical coverage will cover your medical bills, PIP can cover a wider range of costs. Depending on your policy, PIP could cover:

- Lost income as a result of your accident.

- Child care that becomes necessary as a result of your accident.

- Funeral costs if someone passes as a result of your accident.

- Accidental death benefits, which are a lump sum paid to the beneficiaries of anyone who died as a result of the accident. The death must occur in a time frame stipulated within the PIP policy.

- Extraordinary medical benefits, which can cover more expensive and long-term medical expenses incurred by your accident.

Your PIP will cover these costs whether the accident was your fault or not. PIP is typically only required in no-fault states, although not all no-fault states require drivers to have it. Some states don’t allow PIP at all, while others, like Pennsylvania, require it.

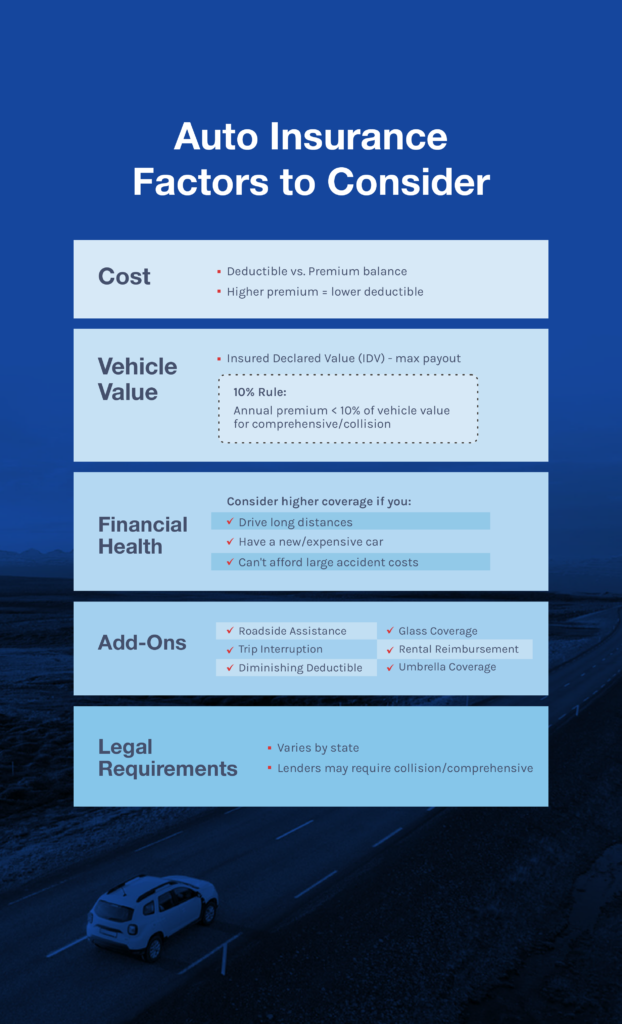

Auto Insurance Factors to Consider

There are several factors to consider about your own situation before you decide which auto insurance type is right for you.

1. Cost

Cost is a top priority when buying auto insurance. One of the first questions to consider is how to balance your deductibles and your premiums. Generally, the higher your premiums are, the lower your deductibles are, and vice versa.

Lowering your premiums means you pay less each month for your coverage. The trade-off is that if you make a claim, you’ll have a higher one-time payment to make for your deductible. When choosing your policy, you must decide whether you prefer the peace of mind that a lower deductible can provide if an accident occurs, or if you’d rather risk a lower premium to try to cut your costs.

2. Vehicle Value

The value of your vehicle may affect the value and type of physical damage insurance you may wish to get.

Your vehicle’s value directly affects the insured declared value (IDV). The IDV is what your insurer believes your vehicle is worth, and is the maximum they’ll pay out to repair or replace it. A higher IDV means your insurer will pay out more for its repairs or replacement, but it does result in higher premiums. Your vehicle’s IDV will usually go down each year as your vehicle depreciates in value.

One common financial guideline that many drivers follow is the 10% rule. This rule states that if your annual premiums will be higher than 10% of your vehicle’s market value, then you shouldn’t get comprehensive or collision coverage. However, this rule is often ignored by those who don’t want to worry about a large and unexpected expense if their car needs to be replaced.

3. Financial Health

Your financial health may also affect which insurance types you need. Insurance is designed to help you pay for high, unexpected costs, and choosing not to get a particular type of insurance could leave you open to covering that cost yourself if needed. If you believe you may not be able to cover a large payment as a result of an auto accident, it’s better to get covered for any costs that are likely to have a large impact on your financial health.

People who should strongly consider a high level of auto insurance are those who:

- Regularly drive long distances.

- Have a new or expensive car.

- May struggle to pay their bills if a road accident means they can’t work.

4. Add-Ons

Many insurance policies come with add-ons that drivers may find valuable. These add-ons can be complementary, or offered for a discounted price. Common add-ons to auto insurance include:

- Roadside assistance coverage: If you become stranded or experience vehicle troubles on the road, you can receive free services to get your vehicle running again or take it to a mechanic. These helpful roadside assistance services include towing, jump-starting, tire changing, fuel delivery and more.

- Trip interruption coverage: If you’re a certain distance from home and your vehicle breaks down, you’ll be covered for lodging or transportation costs. Trip interruption coverage is often paired with roadside assistance.

- Diminishing deductible coverage: Some policies offer to reduce your deductibles by a certain amount for each year that you have no claims.

- Glass coverage: This coverage option will cover the repair or replacement costs of your windshield or windows.

- Rental reimbursement coverage: If having access to a vehicle is a priority, rental reimbursement coverage can cover the cost of a rental car while your damaged vehicle is repaired or replaced.

You can also get umbrella coverage to complement your auto insurance. Often seen as the ultimate add-on to your standard auto insurance, it can cover costs that exceed your standard policy. Additionally, it can sometimes cover costs that aren’t covered by your policy at all. These additional costs are often legal in nature, with your umbrella coverage paying toward legal defense for any lawsuits that arise from an accident you caused.

Umbrella coverage often extends beyond your auto insurance, which means it can cover your home insurance and more. It can also cover legal fees for other types of lawsuit, such as libel or slander. Due to this extensive coverage, umbrella coverage is particularly useful to people with a higher risk of lawsuits or those with more valuable assets. Many auto insurance providers offer discounts on other products and services, too, making their policies even more attractive.

All of these add-ons are valuable perks that may sway which provider you choose. However, they shouldn’t be a key factor in what type of insurance you pick.

5. Legal Requirements

The type of auto insurance required by law varies by state. Almost every state requires some form of liability insurance, although there are nuances involved. For example, in Florida, bodily injury liability is optional under certain policies, but the state requires property damage liability and PIP.

Medical or PIP coverage is required in some states. Collision and comprehensive coverage are rarely, if ever, required by law, but may be required by lenders.

How to Choose an Auto Insurance Policy

Once you’ve researched and compared the different types of auto insurance, you should have the information you need to choose the ideal type for you. To find the right policy for your needs, you should:

- Determine which type of auto insurance you need: Based on the different coverage costs, your vehicle’s value, your financial health and desired add-ons, decide what type of auto insurance you need.

- Choose your coverage level: Decide how much coverage you’ll likely need. This will affect how much you pay in premiums and deductibles, plus how much you can claim.

- Find a reputable insurer: Find an insurer who has a good reputation, meets your needs and is in good financial health.

- Negotiate your policy: Discuss your insurance requirements with an experienced insurance agent before negotiating premiums, deductibles, add-ons and more. By effectively negotiating with your insurance provider, you’re more likely to get the best policy possible.

Finding Your Perfect Auto Insurance

Finding the right type of auto insurance for you is vital to avoiding unexpected costs you can’t afford, complying with your state’s laws and enjoying peace of mind. But to find the perfect auto insurance for your needs, you need to compare the different types.

Each type of auto insurance has something different to offer, meaning you may want or need multiple types of auto insurance. By considering the pros and cons of each, balancing these with your own requirements and then finding a reputable insurer, you’ll soon find your perfect auto insurance policy.